Modern Portfolio Theory: imperfect rationality

Modern Portfolio Theory: imperfect rationality

Portfolio selection in irrational markets

Investors ought to focus on maximizing returns while being exposed to a minimum, or manageable, level of risk. Risk mitigation by applying efficient diversification is therefore of the upmost importance in portfolio construction. Modern Portfolio Theory (MPT), as proposed in 1952 by Harry Markowitz, was a revolution in the field of finance. With the introduction of a quantitative framework for portfolio management, investors were able to optimize their portfolio of assets and manage the trade-off between return and risk (Markowitz, 1952). Relying on a number of assumptions when assessing the level of risk by calculating the standard deviation of returns, MPT has proven to be a valuable tool for investors. However, those assumptions are exactly what caused a dilemma according to a growing number of academics and practitioners, as these often seem unrealistic in real-world scenarios. Whereas this foundation of classical finance theory assumes that markets as efficient and investors show rational behavior, amongst a number of other assumptions, one might ask if this is in line with reality and thus an actual proxy for portfolio construction.

In the mid 70s a new paradigm emerged, arguing that (financial) decision-making is influenced significantly by irrational investment behavior. Backed by research on psychology, two researchers, Amos Tversky & Daniel Kahneman, proposed that cognitive biases have profound impact on our decision-making. This paradigm, knows as behavioral finance, led to Kahneman winning the Nobel Prize in 2002. Behavioral finance challenges the assumptions that were mainstream for so long in classical financial theory. It argues that investors are not always rational and are influenced by cognitive biases (e.g., loss aversion, herd mentality) that can lead to systematic errors in decision making (Shiller, 1984; Tversky & Kahneman, 1974).

The dilemma between MPT and behavioral finance presents the field of finance a significant challenge in portfolio valuation. On one side, MPT offers a normative model for portfolio selection based on rational behavior and market efficiency. On the other side, behavioral finance provides a descriptive model of real-world investor behavior that often deviates from rationality. These conflicting viewpoints on financial theory created a dilemma as finding middle ground and reconciliation has not been an easy task, at least not for the last fifty years. This raises several relevant questions; Should portfolio valuation rely on the rational model of MPT, or should it follow the irrational behavior demonstrated in behavioral finance research? Can these two approaches be reconciled, or are they fundamentally incompatible? Academics have made efforts to combine the two approaches, e.g., by integrating behavioral insights into MPT models. One method was the Adaptive Market Hypothesis (AMH), which suggests that investors are mainly rational, but can quickly show irrational behavior resulting in trading opportunities. According to the AMH, the efficiency of markets is not constant but evolves, influenced by the behaviors and biases of market participants (Lo, 2004).

However, this integration is not without complexities as the original quantitative model of MPT would become more difficult to apply. Furthermore, while Lo acknowledges investor irrationality, the effect is not entirely taken into account. As Rabin (1998) points out, the effects of cognitive biases on asset prices can be much larger than predicted by standard economic models. Several academics further explored the integration of behavioral finance into portfolio theory (Nawrocki & Viole, 2014; Pfiffelmann, Roger, & Bourachnikova, 2016; Shefrin & Statman, 2000) resulting in growing literature on Behavioral Portfolio Theory. These contradicting viewpoints led to an ongoing discussion on the optimal method in portfolio selection, yet the choice for one or the other has significant impact on the risk-return trade-off. A significant complexity lies in the reliability of stock valuation and thus the weight within a portfolio. Presuming that irrational behavior can have an effect on stock prices, in the form of (temporary) over- or undervaluation, should these variances be taken into account? This explorative paper addresses both viewpoints in an attempt to clarify the background and implications of these theories. The deliberate choice was made to focus on a high-level approach of theories and views on risk versus returns as opposed to the many technical elements of portfolio construction. First, in the theoretical section current literature will be explored, including the quantitative framework that acts as the stepping stones of Modern Portfolio Theory. A crucial role is reserved for the assumptions on market conditions that MPT presumes, e.g., risk, costs and information availability. Second, behavioral finance is introduced which led to Behavioral Portfolio Theory (BPT), followed by an analysis of viewpoints. The discussion will further dive into practical implications for practitioners and future research.

Theory

The Mean Variance Theory developed by Markowitz, originated in 1952, provided a framework resulting in an optimal risk-return balanced portfolio. By focusing on the ‘Mean’ of expected returns versus ‘Variance’, i.e., dispersion of returns, otherwise known as risk, investors were able to construct an optimized portfolio. Further referred to as Modern Portfolio Theory, this has proven to be a valuable tool for investors since the 1950s to date.

Yet, MPT has been subject to new insights by researchers and has developed continuously over time. Since then, multiple researchers extended on the original work by implementing factors as market incompleteness, labor income and formula dynamics (Cox & Huang, 1989; Li, Ng, Tan, & Yang, 2006; Merton, 1971). However, evidence presented by Kahneman (1979) indicated that the main element of Markowitz’s mean variance framework, i.e., standard expected utility, does not explain investor behavior (Pfiffelmann et al., 2016). In an attempt to better explain irrational decision-making, Shefrin and Statman (2000) developed the Behavioral Portfolio Theory. The following sections address Modern Portfolio Theory and its counterpart Behavioral Portfolio Theory. An interesting confrontation of viewpoints, backed by decades of research, and where both sides were granted the Nobel Prize for groundbreaking theories. Especially important are the effects, either temporary or not, on individual stock valuations, and thus the effect on portfolio composition, when comparing rational versus irrational decision-making.

Modern Portfolio Theory: 1950 to date

In 1900 a French mathematician, Louis Bachelier, argued that prices will go up or down with equal probability and their volatility could be measured. The distribution of changes in pricing was bell-shaped and large movements were assumed to be extremely rare events (Subathra & Kachi Mohideen, 2017). Based on Bachelier’s work, Harry Markowitz introduced portfolio theory in a Journal of Finance article in 1952. Contrary to investment strategy at the time, which focused mainly on returns as the sum of future expected dividends, Markowitz argued that risk was evenly important. To efficiently manage risk, investors should not invest in one security but construct a diversified portfolio, hence the need for a tool to determine the level of diversification. Markowitz noted that efficient portfolio construction was not mere diversification by adding more assets, but by creating the most optimal combination of assets, risk could be decreased while returns would be maximized under the influence of covariance effects.

Several years later, William Sharpe made an attempt to simplify Markowitz’s model to create a model better applicable for investors. Sharpe argued that a relative small number of variables would lead to the same results as the more complex model of Markowitz (Sharpe, 1963). The introduction of market-models further simplified the mean-variance optimization process. Instead of comparing large datasets of asset pairs, these models offset a specific security against one factor, the broad market index (Lintner, 1965; Mossin, 1966; Sharpe, 1964).

Over time, alternative portfolio theories were introduced focusing on various elements, e.g., skewness (Kraus & Litzenberger, 1976) or a more realistic distribution of returns (Elton & Gruber, 1974; Fama, 1965). Throughout the following years more adaptations of the original theory have been developed by researchers, e.g., how to cope with a single versus multi-period problem increasing uncertainty and complicating estimations (Campbell & Shiller, 1988; Fama, 1970; Hakansson, 1974). This shows the many facets of the mean-variance concept, yet also the possibility for interpretation and a dynamic evolution of the theory.

Portfolio management process

Following Markowitz, the classic MPT investment process can be graphically presented in the following manner.

Figure 1: MPT process

The construction of a portfolio consists of three steps, i.e., 1) security analysis, 2) portfolio analysis and 3) portfolio selection.

Security analysis

The first step focuses on the probability distribution of expected returns, by making a one-time period forecast of the investment opportunity. A plausible investment horizon would be between one month and several years.

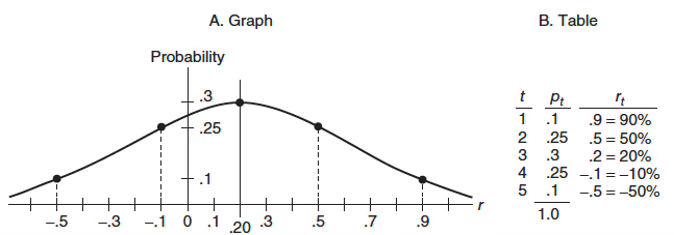

Figure 2: analysis

The analyst should then create a probability of returns for each individual security.

Figure 3: example distribution

Portfolio analysis

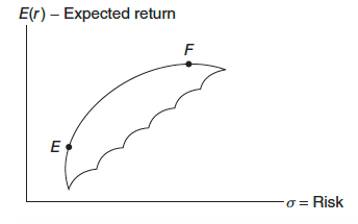

The next step is to enter several statistical inputs to be able to perform a portfolio analysis. These inputs are the expected return, E(r), for every individual security, the standard deviation, σ, and the correlation coefficients, ρ, between all pairs. By analyzing the data under a number of assumptions, further addressed in 2.1.3, the optimal combinations can then be selected. Investors are assumed to pursue either the minimum expected risk at any level of expected return or the maximum expected return at any level of expected risk. If investors, following a given set of assumptions, show logical decision-making behavior a number of efficient portfolios can be plotted, also referred to as the efficient frontier.

Figure 4: efficient frontier

The portfolios on the curved line show the maximum expected return at each risk level. Therefore, the investors’ selected portfolio should be on the efficient frontier. A number of additional tools can be used to define the optimal portfolio, i.e., Capital Market Line (CML) and the Security Market Line (SML) as a representation of CAPM. The CML is used to see a specific portfolio’s rate of return when combined with a risk-free asset while the SML shows a market risk and a given time’s return. CML shows the total risk and measures it in terms of the SML (beta or systematic risk).

Portfolio selection

The last step of the portfolio management process is the actual selection of the optimal portfolio option from the efficient frontier (figure 4). However, ‘optimal’ might differ from one investor to the other as the risk propensity and utility of returns vary between investors (Bell, 1995; Francis & Kim, 2013). Hence, the relevance of behavioral decision-making and the possible effects on assumptions to construct a portfolio.

Assumptions

In order to make the theory ‘work’ and provide a consistent framework for investors, Modern Portfolio Theory is based on a number of assumptions, e.g.:

Cost and capital

Transaction costs and taxes are not taken into account and an unlimited amount of capital can be borrowed at the risk-free rate.

Markets and information

Investors have the same view on expected returns and have access to all information. There are no market inefficiencies, informational asymmetries or changes in economic conditions that could be exploited.

Rationality

Investors are assumed to act fully rational and risk-averse. They will focus on maximizing returns in all situations. Decision-making is solely based on the variability of returns (σ) and expected return [E(r)]. Furthermore, for any given level of risk, investors prefer higher returns to lower returns. Conversely, for any given level of rate of return, investors prefer less risk over more risk.

Distribution

A normal distribution is assumed, making it possible to use various statistical measures, e.g., standard deviation and correlation. All investors visualize each opportunity by a probability distribution of returns that is measured over the same holding period.

Pricing

Single investors are not sizable enough to influence market prices. All investors are equally important in the process.

Criticism

MPT has proven to be a widely used method to construct investment portfolios, its relative simplicity is one the key drivers. However, the used assumptions are prone to criticism towards MPT as they are seen as less applicable in real-world situations. For example, MPT assumes that there are no costs involved in trading, yet trading has significant impact on portfolio returns. Even more, overconfidence and other behavioral biases lead to suboptimal results (Barber & Odean, 2000). MPT also assumes a world of perfect information. Investors have full access to complete information about all available assets, but in reality, information is often asymmetric and costly to obtain resulting in suboptimal performing markets (Leland & Pyle, 1977). Robert Shiller (1981) argued for example that stock prices are more volatile than one would expect, likely caused by imperfect information and investment behavior. Even more relevant, assumptions related to behavior further undermine the validity of MPT.

Investors ought to be rational and risk-averse, yet research on investor decision-making has shown that humans are not fully rational and therefore cannot be assumed to act accordingly (Kahneman, 2011; Thaler, 1980). To be able to use statistical measures a normal distribution of returns is assumed, however, previous research shows that financial returns are often subject to fluctuations not matching normal distribution patterns (Mandelbrot, 1963; Taleb, 2007). While this overview is certainly not exhaustive, the critics on the assumptions functioning as the foundation of MPT are numerous.

Table 1: assumption criticism

Furthermore, a significant issue lies in the risk element, i.e., portfolios are evaluated based on variance rather than downside risk. E.g., two portfolios showing a similar level of variance and returns are considered equally desirable. However, the risk of one portfolio may be subject to frequent small losses, while the other portfolio could suffer from one major loss. It is clear that the element of risk, and more specifically the used definition of risk by the investor, is a major component in portfolio construction. Even Markowitz and Sharpe themselves acknowledged the limitations of MPT. Hence, various scholars and practitioners attempted to create theories better equipped to cope with those limitations.

For instance, one of the adaptations of the original theory was the Post-Modern Portfolio Theory. Rom and Ferguson posited that focusing on downside risk would be a better measure opposed to total variance as investors would happily agree on as much upside volatility as possible.

Figure 5: PMPT frontier

As experiments show, following the PMPT method would lead to improved results in portfolios (Rom & Ferguson, 1991). If changing definitions leads to instant improved returns, the 70-year-old view on ‘optimal portfolio construction’ might be up for debate. New insights and an ongoing discussion on the validity of MPT in ‘real-world’ situations has led to multiple adaptations of the original theory, e.g., the Adaptive Market Hypothesis (AMH) (Lo, 2004) arguing that market efficiency is not stable over time. Other attempts to integrate variable complexities into the original theory are the Black-Litterman model, focusing on subjective views of the investor and forward-looking returns (Black & Litterman, 1991) and Factor-Based Investing looking at various factors, e.g., value and quality not captured by MPT (Fama & French, 1992). In this short explorative study, the choice was made to offset MPT to Behavioral Portfolio Theory (BPT), specifically addressing the irrationality in decision-making of investors, as human behavior is more complex to compensate for and quantify in portfolio construction.

Behavioral Portfolio Theory

Behavioral finance

Studies on decision-making in investment processes have gained growing interest since the 1970s. Especially in the field of behavioral finance, integrating psychology into business and management, valuable insights were provided in an attempt to clarify human behavior and the investor decision-making process. Constraints as informational asymmetries present challenges for investors when making an attempt to assess the level of risk, and thus potential value. In the absence of sufficient information investors often rely on emotionally perceived cues (Franke, Gruber, Harhoff, & Henkel, 2006; Murnieks, Haynie, Wiltbank, & Harting, 2011) or rely on biases and heuristics (Saivasan, 2021; Tversky & Kahneman, 1974). Reasoning from a dual process model, posited by Kahneman (2011), we tend to rely on our emotional System 1 when perceiving risks under uncertainty before our slow and rational System 2 takes over. A process, as shown by decades of research, prone to error due to biases and heuristics resulting in outcomes often deviating from logic.

Risk and returns effects

The main elements of constructing a sustainable portfolio are based on an assessment of expected return (mean) and risk (variance). As systematic, or market, risk cannot be diversified away, investors need to focus on a risk-return efficiency by selecting the most optimal combination of assets.

Figure 6: Risk

Following the assumptions of classic financial theories investors act in a rational manner and focus on maximizing expected utility (Bell, 1995; Nawrocki & Viole, 2014). However, previous research has shown that behavioral biases can lead to a distorted view on risk and return. For example, in Tversky and Kahnemann’s work ‘Prospect Theory: An analysis of decision under risk’ (1979) it is posited that the investors view on value is inconsistent with classic theories. The value function is an S-shaped curve, showing that individuals are risk-averse for gains but risk-seeking for losses. Furthermore, investors tend to be risk-averse when facing gains because of assigning extra weight to small probabilities of large gains but underweight small probabilities of small gains. Conversely, individuals become risk-seeking when facing losses because they overweight small probabilities of small losses but underweight small probabilities of large losses.

Multiple researchers argue that pricing is indeed influenced by biased investors, e.g., for traders experiencing loss-averse behavior and changing their buy and sell contracts accordingly, i.e., selling lower and buying higher (Levy & Levy, 2004; Shiller, 1981). Asset prices that deviated from rational pricing revert quickly to the mean, only creating opportunities for traders able to response quickly. Although only tested on microstructure frequency, it was expected that the results would also apply on lower frequency markets where trader horizons are larger (Coval & Shumway, 2005).

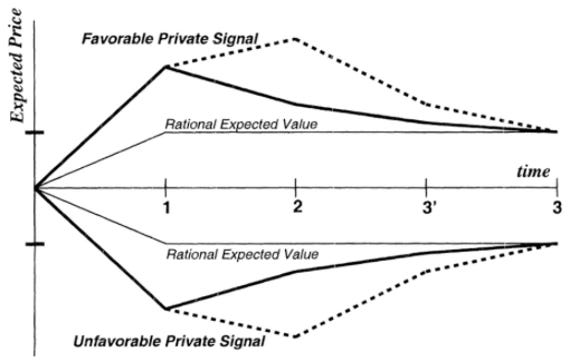

Supporting research on the impact of irrational investor decision-making comes, amongst others, from Daniel, Hirshleifer and Subrahmanyam (1998). They argue that, even though markets are assumed as efficient and incorporate information quickly, decision-making is hindered by a number of biases, e.g., overconfidence and anchoring. This leads to under- or overreactions and challenges the view that securities reflect all publicly available information. The temporary effect is that behavioral biases can have an effect on asset pricing and can be exploited (e.g., arbitrage), but pricing reverts to the mean over time (Barberis, Shleifer, & Vishny, 1998; Daniel et al., 1998).

Figure 7: Divergence & convergence of expected prices under behavioral effects

Behavioral portfolios

Markowitz’s Modern Portfolio Theory has been the cornerstone of research on portfolio selection. The optimal portfolio is a perfectly diversified portfolio of assets where there is a minimum of risk for a given level of expected return. Since the inception in 1952 a number of scholars have extended the framework, for example by adding elements as market incompleteness and labor income. However, not taken into account, until the introduction of the Behavioral Portfolio Theory, was investor behavior.

Portfolios on the BPT efficient frontier are generally not similar to portfolios on the traditional Mean-Variance efficient frontier. As Shefrin and Statman argue, BPT investors construct their portfolio considering other factors, e.g., expected wealth, security and aspiration levels, further supported by research by Levy and Levy (2004) and Das (2010). An experimental BPT construction and its implications are extensively addressed in Shefrin and Statman’s paper ‘Behavioral Portfolio Theory’ and supported in a paper by Pfiffelman et al. (2016). Based on Roy’s (1952) safety-first approach, it implies that BPT investors focus at minimizing the so-called ‘probability of ruin’, or level of loss of wealth, instead of measurement of variance. Optimal BPT portfolios differ from CAPM investors as well. Whereas CAPM centered investors focus on a market portfolio and a risk-free asset, a BPT portfolio shows similarity with a combination of bonds and lottery tickets, also addressed in Prospect Theory (Kahneman & Tversky, 1979; Shefrin & Statman, 2000). It was concluded that their arguments on the support for BPT should be further extended by adding securities of corporations, as well as a period with a longer time-horizon.

On a practical note, the optimal BPT model of Shefrin and Statman (2000) showed that, in over 70% the cases, it is located on the Mean Variance frontier. However, the BPT portfolio also showed high risk and high positively skewed returns (Pfiffelmann et al., 2016).

In their paper ‘Behavioral Capital Asset Pricing Theory’ Shefrin and Statham (1994) further expanded on the classic theory and CAPM by developing the Behavioral Asset Pricing Model (BAPM). They argued that a distinction between two types of traders should be made, information traders and noise traders. In a market fully populated by information traders there is no need for a behavioral theory as price efficiency hypotheses and the CAPM are valid. Concepts as risk premia are solely determined by beta and normal distributions. However, there are also noise traders, not following the CAPM rationality, subject to cognitive errors and lack strict views on mean-variance preferences. Expected returns under the BAPM are determined by behavioral beta, raising issues as these can vary in relatively short timescales, e.g., from month to month (Statman, 1999).

Criticism and limitations

Similar to MPT, BPT also faces criticism. The complexity in quantifying behavior driven motives makes it more challenging to create a consistent framework and limits the practicality in broader investment strategies, hence the standardizing assumptions in MPT. Even more, if all investors would follow an emotional approach, price distortions could be common as proposed by Howard in his paper ‘Behavioral Portfolio Management’ (2014) leading to larger variances.

Information availability is a significant component in efficient construction and assessment of assets and portfolios. As BPT leans into individual differences, perceptions and behavioral assessments, data may be less reliable or harder to replicate. Assigning excessive weight to behavioral factors, as opposed to fundamental analysis, may also lead to suboptimal investment decisions.

Confronting theories

Warren Buffet once said: “MPT has no utility, everybody can do average”. It is safe to say that Warren Buffet has a strong opinion on MPT, and efficient market theory for that matter. However, as argued in the paper ‘The legacy of Modern Portfolio Theory’ (Fabozzi, Gupta, & Markowitz, 2002) MPT has found applications in many aspects of modern finance and its robust framework should grant it a permanent place in portfolio management. Certainly, the widespread usage of MPT selection will make it complex to integrate confronting views on portfolio selection. Even the limited applicability of adapting to real-world situations, investors will probably have a hard time switching to a method prone to be highly individual and less simplistic. Relatively small adaptations to the classic theory aside, the main dilemma lies, as it has done for at least 50 years, in choosing sides. As an investor, are you on the Efficient Markets side or do you follow the Behavioral approach? As it seems even the most influential researchers of the last generations have trouble finding common ground.

Table 2: research efficient markets vs. behavioral finance

When comparing classic Modern Portfolio Theory with Behavioral Portfolio Theory several elements, influencing rational decision-making, are especially important. Two of these closely related elements will be addressed briefly, i.e., utility and expectations on risk and return.

Utility

As a measure of derived happiness, economic theory is based on the assumption that human behavior is ultimately driven by utility maximization. But if we prefer a certain consumer good, or asset for that matter, our personal behavior dictates that we choose the one that delivers the highest level of happiness or satisfaction, either it be chocolate versus strawberries or Tesla stock versus P&G. As MPT assumes that our decision-making is not constrained by, for example, uncertainty, all investors would simply choose the assets with the highest return. However, in the real world where uncertainty is a significant factor, investors can only maximize based on expectations, as nobody knows what the future will bring (Francis & Kim, 2013). Utility is not only driven by what we desire, yet also by risk propensity. Not all investors are created equal and personal risk tolerances vary from one to another (Cummings & Mize, 1969; Highhouse, Wang, & Zhang, 2022),. Even more, biases and heuristics have a profound effect on how we perceive risk (Saivasan, 2021; Tversky & Kahneman, 1974). While MPT does take preferred trade-offs between risk and return into account, e.g., with so-called indifference curves, the subjectivity in the assessment of risk and return can lead to non-standardized results in BPT (Rzepczynski, 2013; Sitkin & Pablo, 1992).

Expectations of risk and return

Traditional portfolio analysis relies heavily on mathematical equations to analyze risk and expected returns. To calculate the expected value on time x several assumptions are used taken a certain probability into account. To be able to find the expected return of an asset MPT relies on historical data and assumes that future projections are stable (Francis & Kim, 2013). In reality though, economic conditions can change dramatically due to unforeseen events creating extreme uncertainty and thus risk (Knight, 1921; Taleb, 2007). Expectations may therefore turn out to be completely unrealistic or unobtainable. Important to note is that this also creates opportunities for either the skilled or the lucky investors.

When related to behavioral driven decision-making an interesting deviation of expectations can occur. In a random game of flipping coins, one would expect that gamblers break even (Francis & Kim, 2013). After all, we assume that there are no distorting effects so chances on either heads or tails should be 50%. Probability theory addresses this concept mathematically in a rational world and relies on, as argued by Cramér, ‘unbiased estimators’ (1946). Conversely, when looking through the lens of prospect theory probability tells us individuals often deviate from rationality and do not make decisions based on objective probabilities. In practice, cognitive biases and emotional reasoning changes our expectations of risk and return. Potential losses and gains are weighted differently and thus influencing how an investor assesses expected future value (Kahneman & Tversky, 1979; Levy & Levy, 2004).

Discussion

Limitations and future research

It seems evident that Modern Portfolio Theory provides interesting angles for sizable studies, hence the vast number of papers dedicated to this field of research. Grasping all elements in detail is therefore an almost unobtainable endeavor in a relatively small study. The goal of this study was therefore specifically not to dive into the many technical calculations and facets used in portfolio selection, but to touch upon the complexities surrounding illogic decision-making and the effects on portfolio risk perception and returns. I am well aware that only the surface of papers in this field of research has been addressed, yet, I am convinced that the current state of literature leaves room for further research.

The adaptable nature of the theory and the significant number of scholars working on the evolution of MPT provides a number of interesting items for future research. Apart from expanding the literature on volatility and pricing under BPT , an interesting possibility for research lies in opportunity timing (period of reverting to the mean) or typologies of investor disposition (Oreg & Bayazit, 2009) to create a variable framework for behavioral investors.

In my personal opinion one particular concept connecting MPT and BPT could be well worth a more thorough future study. Previous research showed that there is correlation between informational availability and biased behavior revealing a double research opportunity. First, as Statman (1999) stated, in a world populated solely by information traders, i.e., acting on full informational availability, all assumptions on beta, CAPM and distributions hold. However, for so-called noise traders, trading on limited informational availability, this is not the case. Noise traders tend to act irrationally, emotion-driven and show herd behavior. Due to this behavior, they can cause price and risk levels to diverge from expected levels even if all other traders are rational. Acknowledging that biases and heuristics are a factor to cope with for all investors, it might be interesting to research the effect of convergence over time. Can investors comply with general MPT assumptions if there is sufficient information and if yes, where does the tipping point lie when irrational behavior is replaced with rational decision-making?

Second, and closely related, is the efficiency and performance of portfolios by informed and noise traders. If information is in the phase of being asymmetric or insufficient a portfolio could still perform well, it is either a matter of skill or luck. Many retail traders overestimate their own capabilities resulting in high loss ratios. However, if they belong to the few that do perform well their cognitive biases will be confirmed possibly leading to more trades with larger variances. As bias-driven portfolios tend to have larger variances, one could ask if irrationality needs to be compensated.

Figure 8: Availability-performance matrix

Conclusion

The opposing standpoints of adepts of efficient markets versus behavioral investors has been an interesting debate during the last 50 years and it is not expected that this will change in the near future. The question remains; what method is best? Even after decades of research, the current state of literature is not able to provide a one-size fits all solution. Modern Portfolio Theory delivers a solid mathematical model that is widely used, despite its shortcomings of unrealistic assumptions. Behavioral Portfolio Theory takes all sorts of biases into account, providing an explanation for divergence of asset pricing, but relies on a more individual portfolio selection preventing the model to be applicable on a unified scale.

As Antony (2020) states, behavioral finance can complement classic finance theories. The behavioral portfolio model can give a prescriptive approach by integrating psychology and practitioners can provide insights and self-control for decisions made by clients. On a more practical side, that is in actual trading, information traders, following all assumptions in a rational world, and noise traders could be in for a confrontation. According to Shefrin & Statman (1994) these traders, not limited by the boundaries of rational assumptions, can generate a shock and indeed influence asset pricing.

Human behavior and irrational decision-making are, according to my opinion, factors not easy to disregard. In a perfect world with full informational availability and a market without distorting biases it makes sense to blindly follow Modern Portfolio Theory, no questions asked. However, as research shows, there is indeed a risk and return effect in the form of mispricing and larger variances. There certainly is moderate consensus on the timing effects of affected pricing. In due time prices tend to revert to the mean and follow fundamental analysis. For long term investors MPT does therefore not seem to be outdated yet. This does not mean that there is no room for Behavioral Portfolio Theory, on the contrary. In practice, BPT can be extremely useful in explaining price difference in the diverged asset pricing period and create possible arbitrage opportunities for some investors, either skilled or lucky.